05.07.24

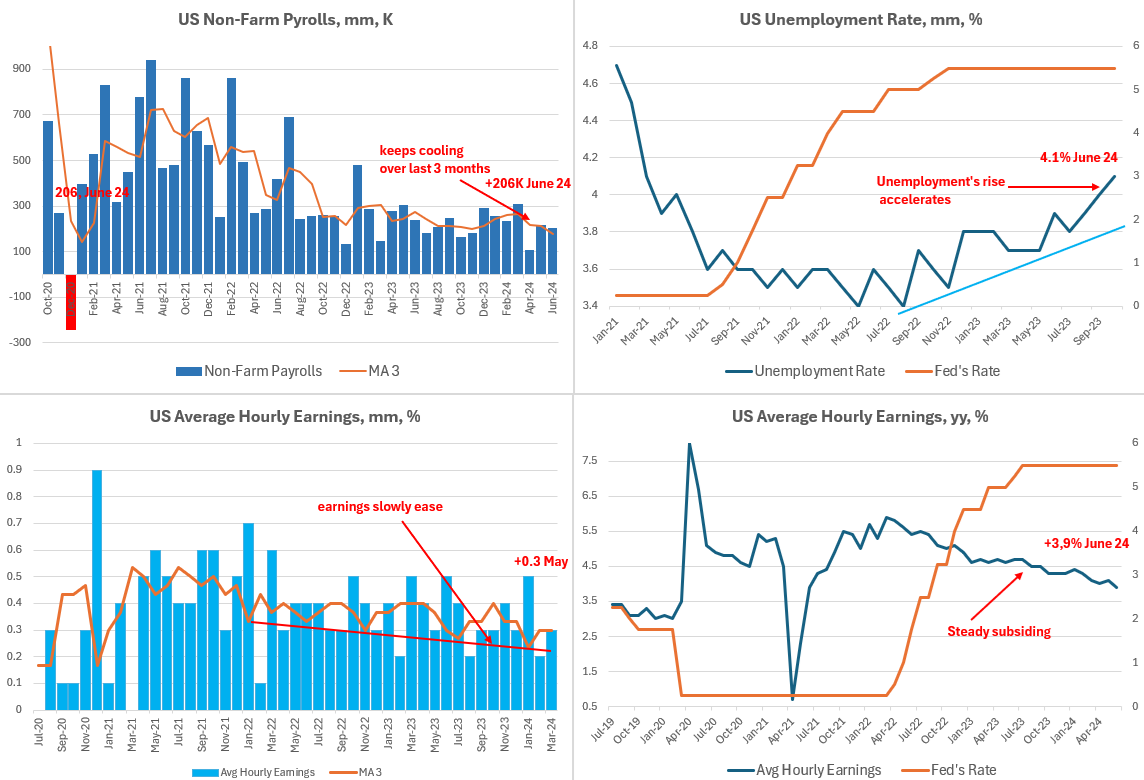

The number of new jobs in US nonfarm sector increased by 206.000 in June, in line with the current trend which is now creeping lower than in 2021 and 2022 when the numbers of 300.000 per month were not rare case. However, the result of previous months was revised down by total 111.000 jobs and this caused 3-months moving average to descend to 177.33 (see chart) which is the weakest result since January 2021. Fewer jobs mean less earnings and consequently less spending by consumers. That is bad for economy but positive for inflation prospect which is a concern for Fed and is supposed to cool as a result of labor market easing.

Another sign of labor market cooling is an unemployment rate increasing to 4.1% in June – the record from November 2021. The upward dynamic of unemployment rate is now clearly accelerating (see chart) which is again good sign for inflation but on the other hand poses risks of recession in the economy. What if this cooling does not stop in timely manner?

Average hourly earnings increased by 0.3% in June from May and by 3.9% from year earlier, which is the slowest pace from the spring of 2020. This again confirms inflation is on its way to 2% target and gets Fed closer to start easing policy, maybe as soon as in September.

Meanwhile speculations intensify about the timing of possible rate hike. Fed insists it will be based solely on economic data and in no case tied to political events.

Next important data on inflation will be published on Thursday July 11 and will be watched carefully by the market to get further insights for possible timing of policy easing start.

On the last meeting in June Fed left its rate unchanged and adjusted projections for only one rate cut this year from three cuts before. Taking into account last data showing inflation and labor market are easing markets now started to hope for two cuts.